€7.67 Meal Allowance: How to Make the Most of It (2026 Playbook)

1. Claim the full rate instead of halving it

Making the most of the meal allowance starts with a simple realization: most companies don't claim the full amount. They grant only the benefit-in-kind value and leave the tax-free top-up unused.

The maximum tax-advantaged amount in 2026 is €7.67 per working day. It consists of the benefit-in-kind value (Sachbezugswert) of €4.57 plus an additional employer top-up of up to €3.10. Apply only the €4.57, and about 60% of the available lever reaches the team, while the rest stays on the table.

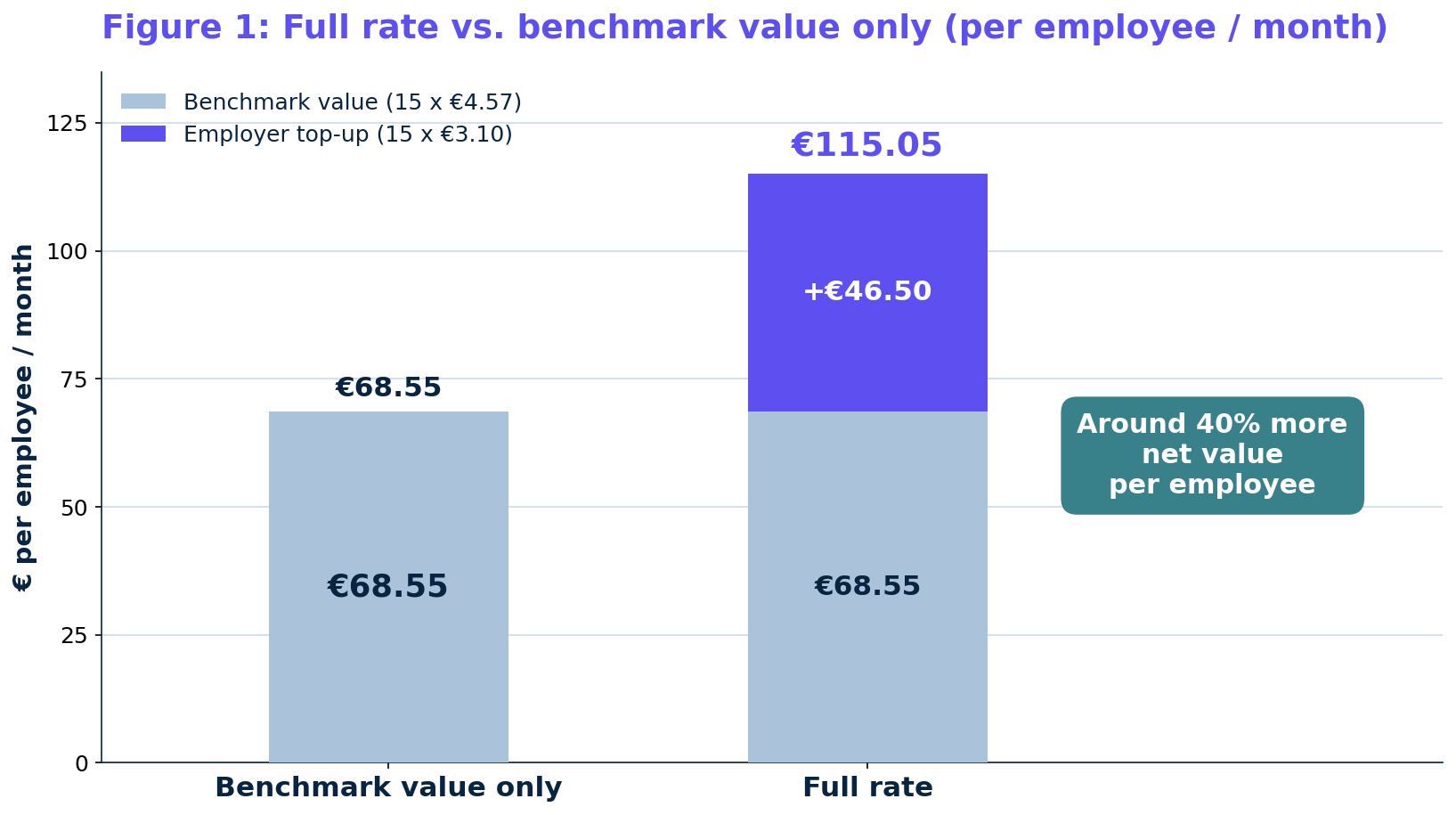

The difference is concrete. Over 15 working days that's €68.55 instead of €115.05 per employee per month. Per head, around €46.50 a month goes unused. Across a 100-person team, the foregone value adds up to roughly €4,650 a month, or nearly €56,000 a year.

Figure 1: Meal allowance per employee per month over 15 working days. Benchmark value only (€4.57/day): €68.55. Full rate (€7.67/day): €115.05. The additional employer top-up of €46.50 a month lifts around 40% more net value.

Note that the full rate doesn't automatically cost the employer more out of pocket. Part of the amount is carried by the employee's own contribution. For exactly how the figure is built, see our guide on calculating the 2026 meal allowance. For how the allowance fits into total catering spend, see the guide to catering costs for companies.

2. Apply the 15-day rule correctly

The allowance is tied to working days. Each month you can apply a flat 15 working days without itemizing every single meal. This flat figure keeps the benefit lean in payroll.

These 15 days are the standard for full-time staff and remove the need for daily checks. Two conditions remain: a maximum of one meal per working day, and no reimbursement on vacation or sick days. Meet both, and the accounting rests on a clean, audit-proof basis.

For part-time staff or low on-site presence, it pays to look at the actual working days. Applying a flat 15 days when someone only works eight days a month risks corrections in a payroll audit. For most full-time teams, though, the 15-day flat rate is the simplest and cleanest route.

One common mistake: the amount applies per day, not per month. Misreading €7.67 as a monthly figure underestimates the volume by a factor of 15. The flat rate doesn't cap the month; it simply streamlines how the individual days get accounted for.

3. Set the employee share right

The biggest lever for tax exemption is the employee's own contribution. Whether any tax applies at all hangs on it.

If the employee pays at least €4.57 per meal themselves, no taxable benefit remains. The allowance is then fully tax-free, for the employer too. If the contribution is lower, a flat 25% tax applies to the benefit-in-kind value. The €3.10 top-up portion stays tax-free in both cases.

A quick example makes the logic clear. If lunch costs €9 and the employee pays €4.57, the employer covers €4.43. Because the contribution exactly matches the benefit-in-kind value, nothing is taxable. If the employee pays only €2, a taxable benefit arises equal to the benefit-in-kind value, which the employer taxes at a flat 25%.

The optimal setup is therefore one where the meal costs more than €4.57 anyway, which is practically always the case at lunch. That way the full allowance flows tax-free and the admin stays minimal. Social contributions don't apply in any of these cases when the daily setup is correct.

Meal allowance and catering from a single source

- Full €7.67 rate properly claimed

- Combination of allowance and catering

- Tax leeway reviewed

- Matching caterers for on-site days

4. Combine with catering instead of either-or

The allowance rarely delivers its biggest effect on its own. It comes into its own in combination with other catering building blocks, a mix that hybrid teams in particular benefit from.

On on-site days, plannable office catering provides shared meals in the office. On remote days the allowance kicks in, because it works regardless of location. That way every working situation gets the right offer, without overstretching one model.

The combination also makes economic sense. Instead of ordering catering every day that nobody calls up from home, you pay deliberately for on-site presence and use the flexible allowance for the rest. A team with three office days and two remote days covers the office days through the caterer and the rest through the allowance, with no idle cost.

It also feels stronger in perception. Shared meals on office days strengthen the team; the allowance on remote days signals appreciation beyond the office too. For how catering breaks down per head, see our piece on catering cost per employee.

5. Choose the right redemption tool

How well the allowance gets used depends heavily on the redemption route. Paper meal vouchers are cumbersome and expensive to handle; digital solutions clearly win out.

A good app captures receipts by photo, checks them automatically, and assigns them to the relevant working day. Billing flows straight into payroll. That cuts the effort for HR to a few minutes a month and takes the risk out of the flat-rate taxation.

When choosing, watch for three things: automatic receipt checking, a clean interface to payroll, and easy operation for employees. The smoother the redemption, the higher the adoption, and the more impact the benefit delivers. A solution that accepts receipts from the supermarket, delivery service, and restaurant alike best covers real eating habits.

Location independence comes on top. If you have employees working from home, in the field, and across multiple sites, the tool has to work the same everywhere. Digital redemption beats location-bound options like a classic canteen on precisely this point.

6. Secure adoption: how your team really uses the allowance

An allowance nobody redeems fails as a benefit. It stays an unused line in payroll. Adoption decides the impact, not the theoretically possible amount.

Two levers and one habit drive adoption. First, clear communication: the team needs to know that the allowance applies every working day and how to redeem it. Second, a simple app that works in under a minute per receipt. And third, regularity, so redemption becomes routine rather than slipping the mind at month-end.

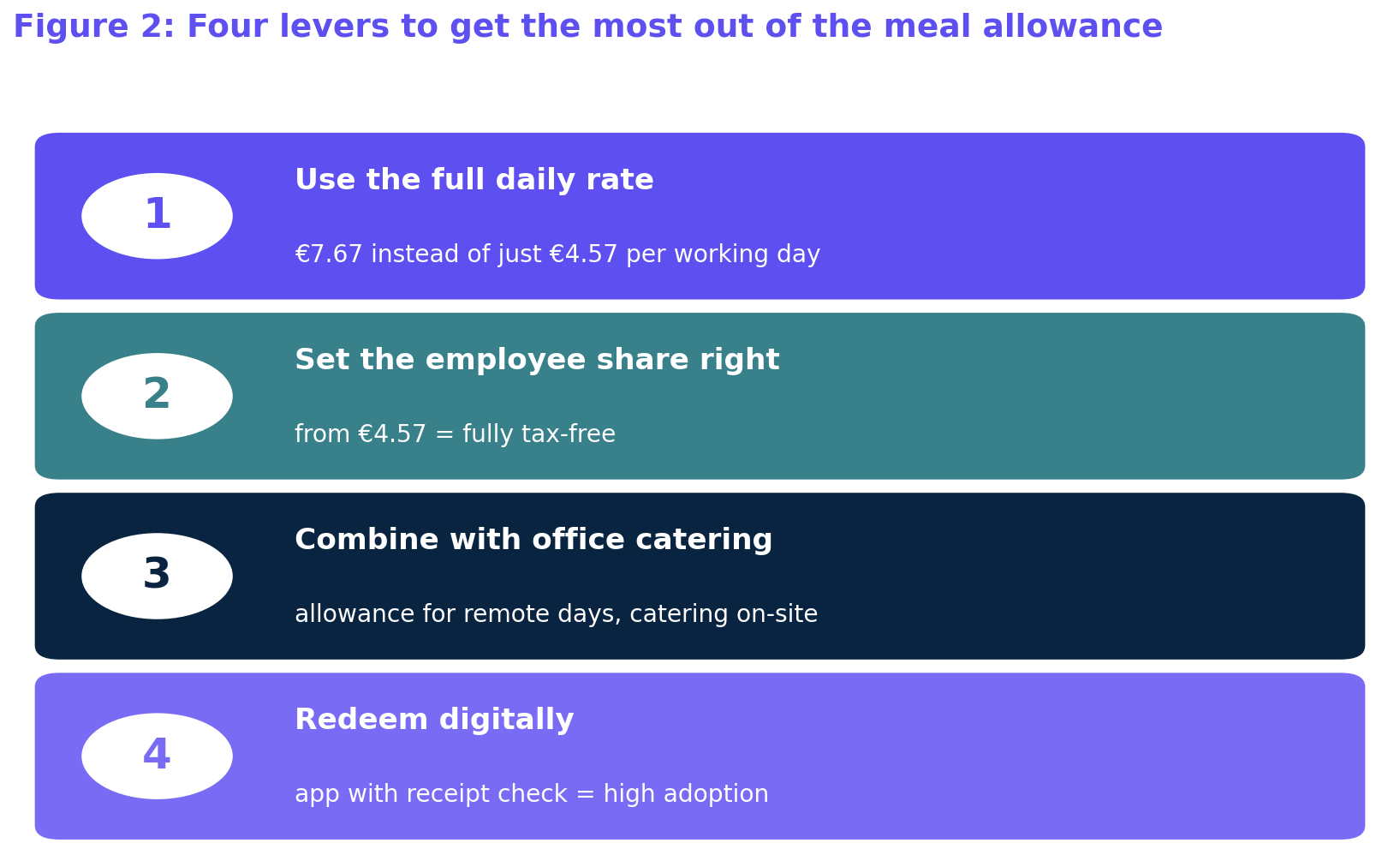

Figure 2: Four levers for optimization. Use the full daily rate of €7.67. Set the employee share from €4.57 for full tax exemption. Combine with office catering on on-site days. Redeem digitally for high adoption.

A short onboarding note and an intranet FAQ are usually enough to establish usage. It also helps to explain the allowance to new hires right when they join, rather than weeks later. For the strategic picture, see our complete guide to employee catering.

7. Common mistakes that cost the lever

Three mistakes cost real money or nerves in practice, and all three are easy to avoid.

First: applying only the benefit-in-kind value. Leaving out the additional €3.10 top-up means using only €4.57 instead of €7.67 per day, giving away around 40% of the lever. This one costs the most and shows up the most often.

Second: paying irregularly. An allowance that comes some months and not others doesn't work as a reliable benefit. The effect on satisfaction and retention only builds with steady usage over several months.

Third: sloppy documentation. Without working-day receipts, the flat-rate taxation wobbles in an audit. An app with automatic receipt checking removes that risk and makes the effort predictable.

Avoid these three points, and you extract the full potential from the allowance, turning it into a benefit that genuinely lands.

Start a no-obligation needs analysis

- Tax-advantaged volume calculated for your team

- Comparison of allowance, catering, and the mix

- Accounts for locations and on-site ratio

- Result within a few hours

Conclusion

Making the most of the meal allowance isn't a question of complex tax models, but of consistent application. The full rate of €7.67, a cleanly set employee share from €4.57, the combination with catering, and simple digital redemption together get the maximum out of the benefit.

The difference between half and full usage is around 40% more net value per employee, at the same base effort. Across a 100-person team, that's roughly €4,650 a month. Concretely: in the next payroll run, check whether the additional €3.10 per day is actually being applied, and add it if the €56,000 a year is still sitting unused.

FAQ

How do I claim the full meal allowance?

Apply the full daily rate of €7.67, not just the benefit-in-kind value of €4.57. The additional employer top-up of €3.10 is tax-free and lifts around 40% more net value per employee, about €46.50 more a month.

Why does the allowance stay tax-free with an employee share from €4.57?

Because no taxable benefit remains. The contribution matches the benefit-in-kind value, so there's nothing to tax. Below that, a flat 25% tax applies to the benefit-in-kind value; the €3.10 top-up stays tax-free.

Is the allowance worth it alongside office catering?

Yes, especially for hybrid teams. A caterer delivers on on-site days, and the allowance covers remote days. That way every working situation gets a fitting offer, without overloading one model or creating idle cost.

How do I increase adoption in the team?

With clear communication, a simple receipt-capture app, and regularity. The smoother the redemption, the more employees actually use the allowance. An onboarding note at joining and a short intranet FAQ usually do the job.

How many days a month can I apply?

A flat 15 working days, without itemized proof. A maximum of one meal per working day is eligible, and there's no reimbursement on vacation or sick days. For part-time staff it pays to look at the actual working days.

What does the full rate deliver across a whole team?

For 100 employees over 15 working days, the tax-advantaged volume is €11,505 a month. Applying only the benchmark value gives €6,855. The difference of around €4,650 a month is the lever that stays unused at many companies.

Similar articles

Get an individual menu suggestion today.