Meal Allowance 2026: How to Calculate It, With Worked Examples

1. Meal allowance 2026: the key numbers

The 2026 meal allowance isn't one pot of money. It's a tax construct with two building blocks. Know both, and your budget math is clean.

Block one is the official benefit-in-kind value for a lunch. In 2026 it rises to €4.57 per working day. Block two is a tax-free employer top-up of up to €3.10 on top. Together they make the headline figure of €7.67 per working day.

This amount is per employee and per working day, not per month. For payroll, you can apply a flat 15 working days a month without proving each individual meal.

The value edged up in 2026 because the benefit-in-kind rate is adjusted to consumer prices each year. For budgeting, that means one thing: check the current rate once a year, then your calculation holds. Plan with stale figures and you'll plan too low.

Figure 1: How the 2026 tax-free meal allowance is built. Benefit-in-kind value €4.57, employer top-up €3.10, up to €7.67 per working day, about €115 per employee per month over 15 days.

For the strategic picture, see our complete guide to employee catering.

2. How the meal allowance is taxed

The tax treatment hinges on one number: the employee's own contribution. That decides whether any tax applies at all.

If the employee pays at least €4.57 toward each meal, no taxable benefit is left. The allowance is then fully tax-free, for the employer too.

If the contribution is lower, the employer taxes the benefit-in-kind value at a flat 25%. The €3.10 top-up stays tax-free either way. Social contributions don't apply when the day-based setup is correct.

A quick example makes it click. Say lunch costs €9 and the employee pays €4.57. The employer covers €4.43. Since the contribution matches the benefit-in-kind value exactly, no taxable benefit remains and the allowance is fully tax-free.

If the employee pays only €2, a taxable benefit arises equal to the benefit-in-kind value. The employer taxes it at a flat 25%. The perk still lands net for the team.

Documentation matters. The allowance is day-based, covers one meal per working day, and doesn't apply on holiday or sick days. In home office it still works through digital receipts.

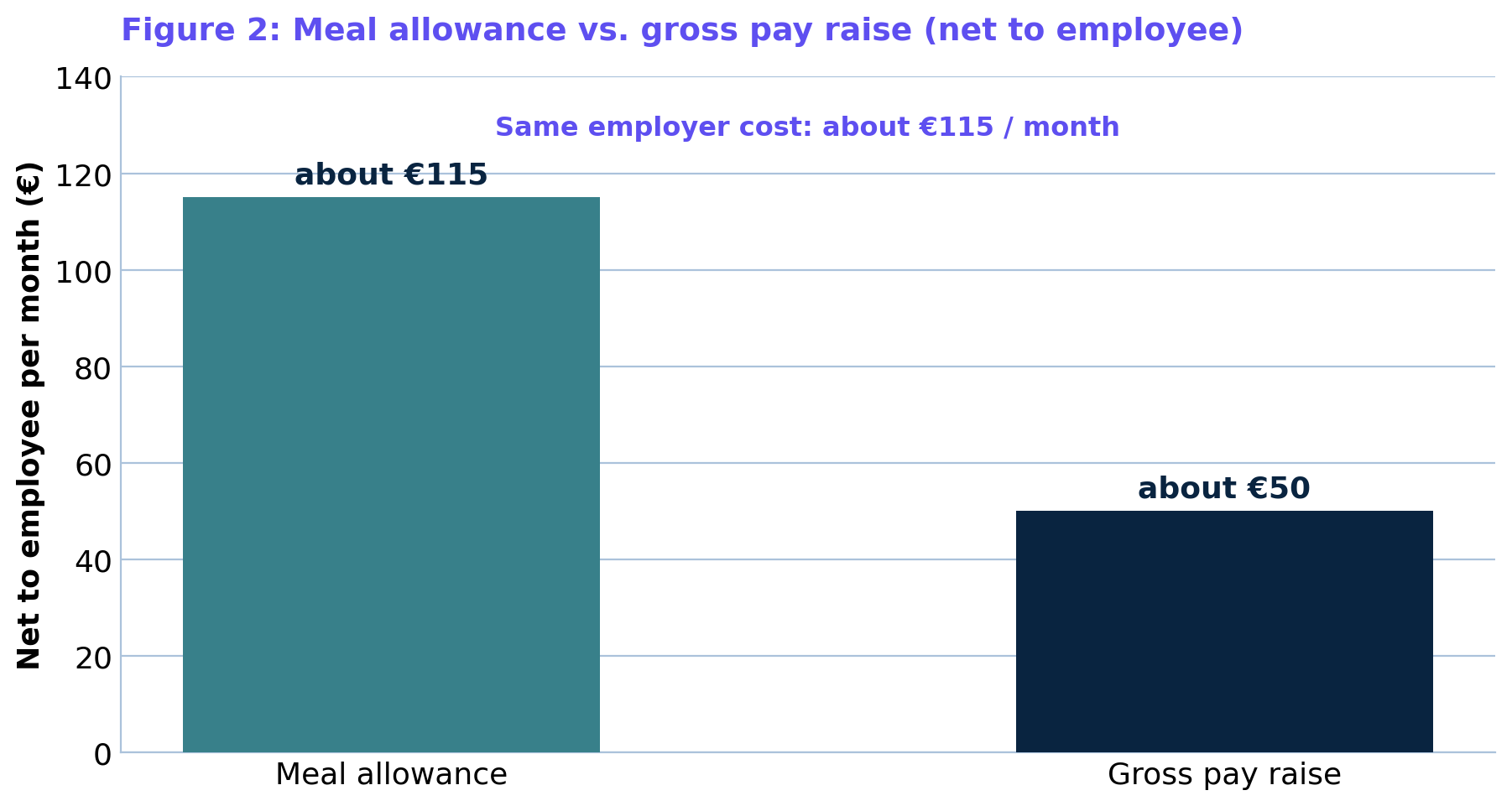

3. Meal allowance vs. a pay raise: what delivers more

A pay raise sounds generous, but a big chunk evaporates in tax and social contributions. That's exactly where the meal allowance wins.

For the same employer spend, far more reaches the team through the allowance, because it isn't taxed like gross salary. A raise gets taxed and charged for social contributions, on both the employee and the employer side.

Figure 2: Meal allowance vs. gross pay raise, simplified example at about €115 of employer spend per month. Net to the employee: about €115 via the allowance, about €50 via a pay raise (assuming roughly 50% deductions). The allowance delivers more than double the net value.

For how levers like this fit into total cost, see our guide to catering costs for companies.

4. How to calculate it, step by step

The math is simpler than it looks. Three steps give you the monthly volume per employee.

Step one: set the daily maximum. That's €7.67 (€4.57 benefit-in-kind value plus €3.10 top-up).

Step two: multiply by the applicable working days. The flat rate is 15 days a month. Result: 15 times €7.67 is €115.05 per employee per month.

Step three: scale by headcount. For 100 employees, that's a tax-advantaged volume of €11,505 a month (100 times 15 times €7.67).

Set the allowance lower, say only the benefit-in-kind value without the full €3.10 top-up, and you leave tax savings on the table. For a detailed budget logic by team size, see our piece on catering cost per employee.

Meal allowance and catering from one source

- Tax options reviewed

- Allowance and catering combined

- A realistic budget estimate

- Matched caterers for any team size

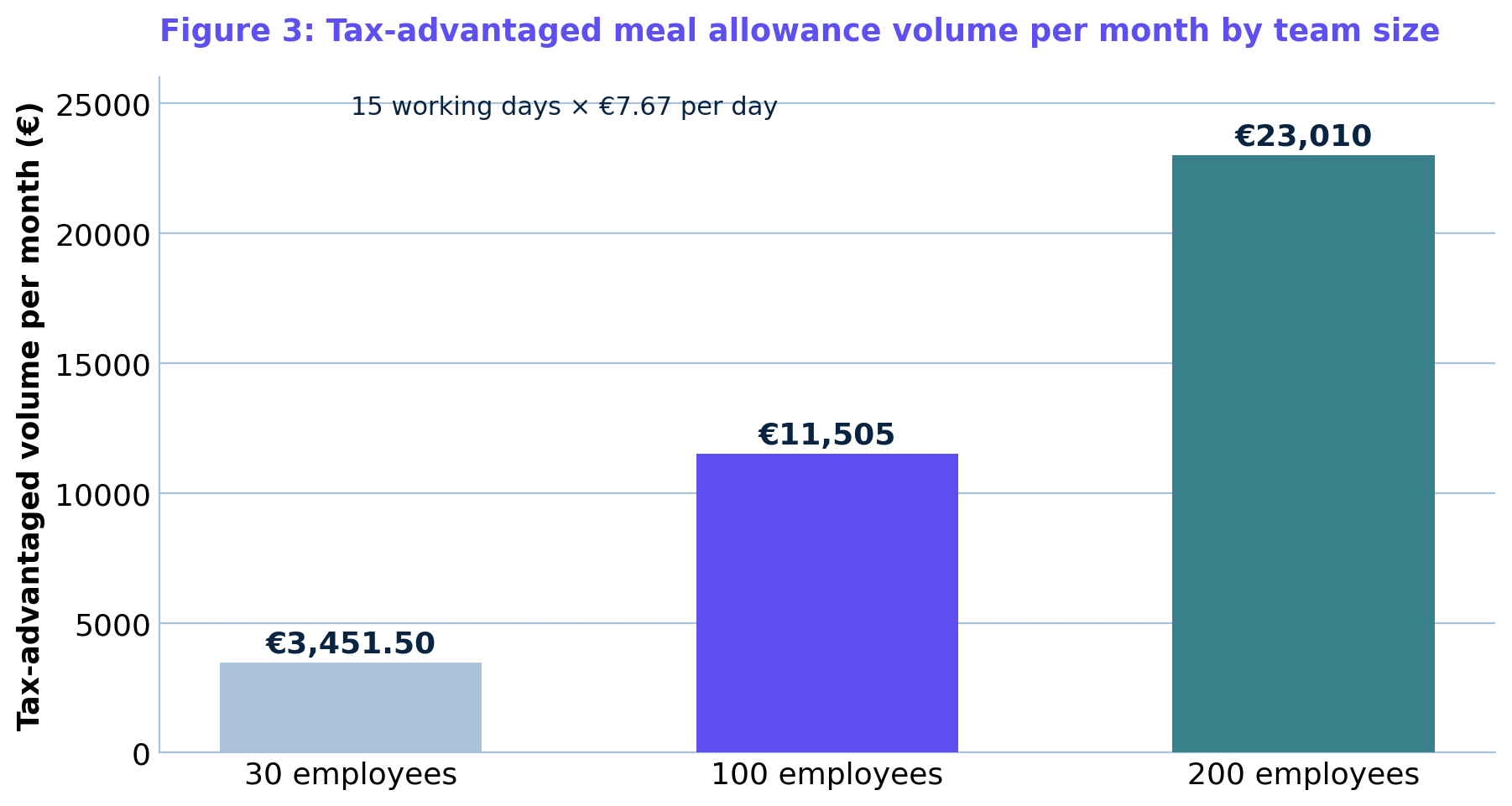

5. Worked examples: 30, 100, and 200 employees

Theory is fine. Hard numbers are better. The examples below calculate the monthly tax-advantaged volume at the full allowance over 15 working days.

A team of 30 reaches a tax-advantaged volume of €3,451.50 a month. That's 30 times 15 times €7.67.

A mid-sized company with 100 employees lands at €11,505 a month. That exact amount flows tax-advantaged and reaches the team net.

A site with 200 employees comes to €23,010 a month. Over a year, that's a tax-advantaged volume of about €276,000.

Typical setups sit behind those numbers. A 30-person startup with a high home-office share runs the allowance purely digitally, because it works from home too and needs no caterer. The effort stays minimal, the benefit is still visible.

A 100-person mid-sized company on a fixed site often blends. A caterer delivers on office days, the allowance covers home-office days. Each group gets a fitting offer, and no single model gets stretched.

A large 200-person site uses the allowance as a baseline for everyone and adds regular catering on in-office days. The €23,010 monthly volume is the ceiling that can be lifted tax-side.

Figure 3: Tax-advantaged meal allowance volume per month by team size, at 15 working days and the full €7.67 daily rate. 30 employees: €3,451.50. 100 employees: €11,505. 200 employees: €23,010.

These figures are the tax-advantaged volume, not the raw cost. Part comes from the employee's own contribution, the rest from the employer. The right mix depends on team size and attendance. For fixed sites, it pairs well with office catering.

6. How to roll out the meal allowance

Rollout is almost always digital now. Paper meal vouchers are the exception; apps with receipt capture are the standard.

The flow is lean. Employees photograph a receipt from the supermarket, a delivery service, or a restaurant. The app checks it and assigns it to the working day. Billing flows automatically into payroll.

Sort out three things first. One: a single meal per working day. Two: no reimbursement on days off. Three: clean documentation, so the flat-rate taxation holds.

For hybrid teams the allowance is ideal, because it works anywhere. If you also want hot food on office days, pair it with predictable catering through a marketplace.

The admin load stays light. Setup takes a few days, and monthly upkeep is just approving the captured receipts. For HR and finance that's far leaner than running a canteen, and more predictable than ad-hoc food orders with no system.

Clear communication to the team matters. People who know the allowance applies daily and how to redeem it actually use it. A short onboarding note and an intranet FAQ usually do the job.

Get a free needs assessment

- Tax-advantaged volume calculated for your team

- Allowance, catering, and blend compared

- Factors in sites and attendance

- Result within a few hours

7. Common meal allowance mistakes

Three mistakes cost real money or real hassle.

First: applying only the benefit-in-kind value. Drop the extra €3.10 top-up and you use just €4.57 instead of €7.67 a day, leaving about 40% of the lever unused.

Second: paying it irregularly. An allowance that comes and goes doesn't land as a reliable benefit. The effect on satisfaction and retention only shows with steady use.

Third: sloppy documentation. Without day-based receipts, the flat-rate taxation gets shaky. An app with automatic receipt checks removes that risk.

Avoid those three and you get the full value from the allowance.

The bottom line

The 2026 meal allowance is the most tax-efficient food benefit companies have right now. At €7.67 per working day, used in full over 15 days, about €115 per employee per month reaches the team almost entirely net.

The lever works hardest when you use the full rate and document it cleanly. Apply only the benefit-in-kind value, or pay irregularly, and you leave money behind. Run the volume for your team size once, and the decision is clear.

FAQ

How high is the meal allowance in 2026?

Up to €7.67 per working day is tax-advantaged. The figure combines the benefit-in-kind value of €4.57 and an employer top-up of €3.10.

Is the meal allowance tax-free?

With an employee contribution of at least €4.57 per meal, it's fully tax-free. Below that, a flat 25% tax applies to the benefit-in-kind value. Social contributions don't apply when it's set up correctly.

How many days a month does it cover?

You can apply a flat 15 working days a month without itemizing each meal. One meal per working day is eligible.

Does the meal allowance work in home office?

Yes. Through digital receipt capture, employees redeem it anywhere, including from home. There's no reimbursement on holiday or sick days.

What does the allowance deliver versus a pay raise?

For the same employer spend, far more reaches the team net, often more than double, because there's no income tax and no social contributions like there are on gross salary.

How do I calculate the volume for my team?

Multiply €7.67 by 15 days and your headcount. For 100 employees, that's €11,505 a month in tax-advantaged volume.

Similar articles

Get an individual menu suggestion today.